If your organization operates across the UK and EU, you've likely run into both acronyms — and the confusion between them is genuinely common, because they cover similar ground (energy and carbon disclosure) but differ in scope, jurisdiction, and requirements. Getting this wrong isn't just a paperwork problem; reporting under the wrong framework, or missing one you're actually in scope for, creates real compliance risk.

CSRD (Corporate Sustainability Reporting Directive) is an EU-wide sustainability disclosure requirement covering environmental, social, and governance data for companies operating in or connected to the EU. SECR (Streamlined Energy and Carbon Reporting) is a UK-specific requirement focused narrowly on energy use and carbon emissions for qualifying UK companies. They are not interchangeable, and many organizations are in scope for both.

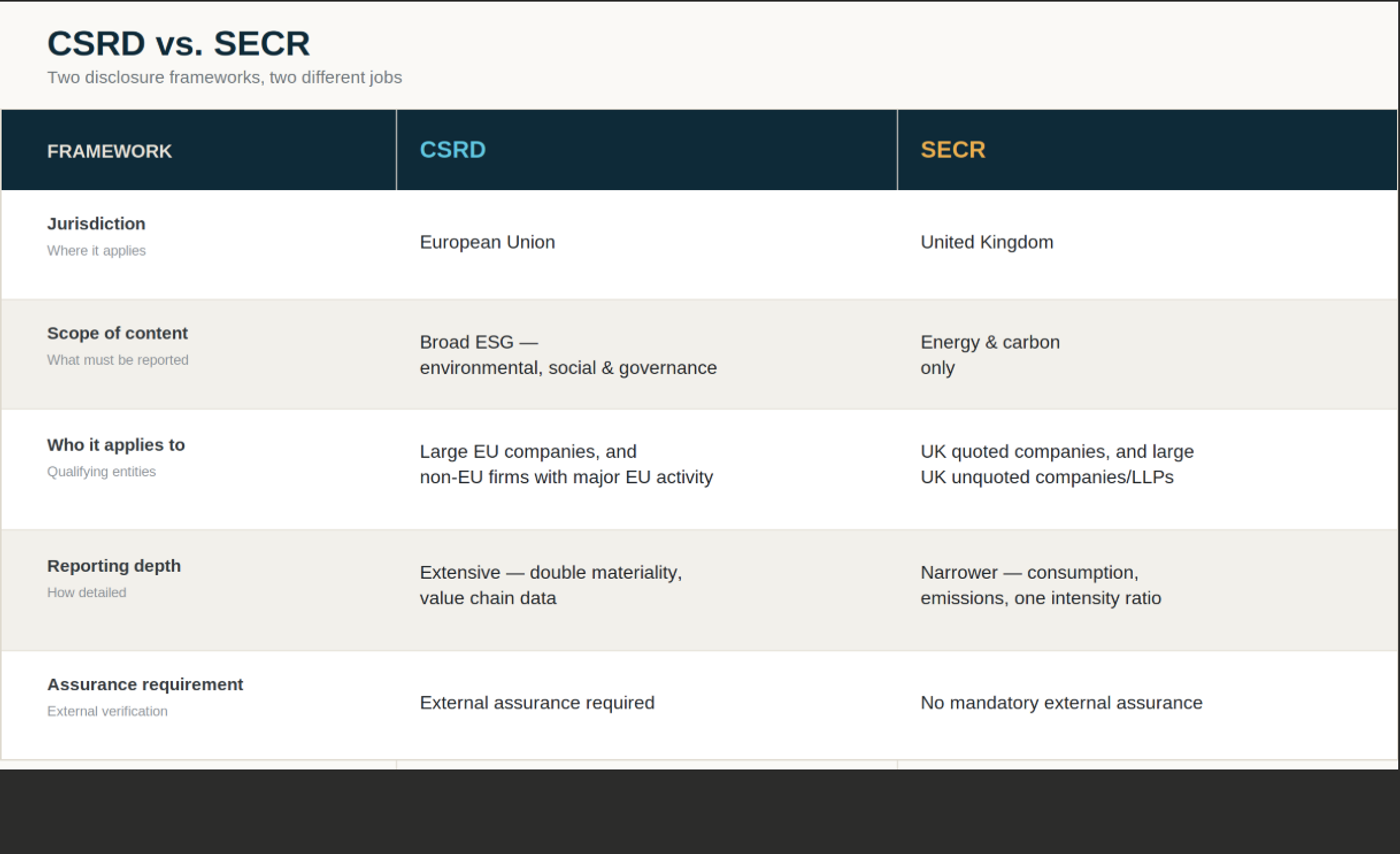

What CSRD actually requires

CSRD replaced and significantly expanded the EU's earlier Non-Financial Reporting Directive. It requires companies to report using the European Sustainability Reporting Standards (ESRS), covering far more than energy — climate, biodiversity, workforce, human rights, governance, and business conduct all fall within scope. A key concept unique to CSRD is double materiality: companies must report both how sustainability issues affect their business, and how their business affects the environment and society.

CSRD applies in phases based on company size, with large EU companies going first and non-EU companies with substantial EU turnover or EU-listed securities brought into scope in later phases. This is the detail that catches many non-EU companies off guard — CSRD isn't limited to companies headquartered in the EU.

What SECR actually requires

SECR is far more contained. Introduced in 2019, it requires qualifying UK companies to report:

- UK energy use (as a minimum, electricity, gas, and transport fuel)

- Associated greenhouse gas emissions

- At least one intensity ratio (emissions relative to a business metric, like per employee or per unit of revenue)

- A narrative on energy efficiency actions taken during the year

SECR applies to UK quoted companies of any size, and large UK unquoted companies and LLPs that meet at least two of: over 250 employees, over £36m turnover, or over £18m balance sheet total. It's reported as part of the annual Directors' Report, not a standalone sustainability disclosure.

The overlap that trips people up

A UK subsidiary of a large EU-connected group can easily be in scope for both: SECR because it's a qualifying UK entity, and CSRD because its parent group meets EU thresholds and CSRD often requires consolidated group-level reporting that pulls subsidiary data upward. In that situation, the same underlying energy and emissions data needs to satisfy two different frameworks with two different required formats and audiences — which is exactly where duplicated manual effort creeps in if the underlying data isn't structured to serve both from the start.

Practical takeaway

- If you're UK-based and meet the size thresholds: you likely need SECR, regardless of EU activity.

- If you're EU-based, or a non-EU company with material EU operations or listings: you likely need CSRD, which will demand far more than SECR alone.

- If both apply: the efficient path is maintaining one clean, granular dataset of energy consumption and emissions that can be sliced to meet each framework's specific format, rather than building two separate reporting processes from scratch.

That last point is where automated, audit-trail-backed emissions tracking earns its keep — ecolyptus's Sustainability Footprint and reporting tools are built to produce both CSRD and SECR disclosure-ready exports from the same underlying GHG Protocol-aligned data, rather than treating them as two unrelated reporting exercises.

FAQs

Do I need to comply with both CSRD and SECR? Only if you meet the qualifying criteria for both — commonly the case for UK subsidiaries of larger EU-connected corporate groups, but not automatic just because a company operates in both regions.

Is SECR being replaced by CSRD? No. SECR remains a distinct UK requirement; CSRD is an EU directive. The UK is not bound by CSRD post-Brexit, so SECR continues to apply on its own separate basis.

Does CSRD apply to companies outside the EU? Yes, in certain cases — non-EU companies with significant turnover generated in the EU, or with securities listed on an EU-regulated market, can fall into CSRD's scope even without EU headquarters.

What happens if a qualifying company doesn't comply? Requirements and enforcement mechanisms differ by framework and jurisdiction, and can include financial and legal consequences — this is worth confirming with a compliance or legal advisor specific to your situation, since enforcement details fall outside general guidance like this.